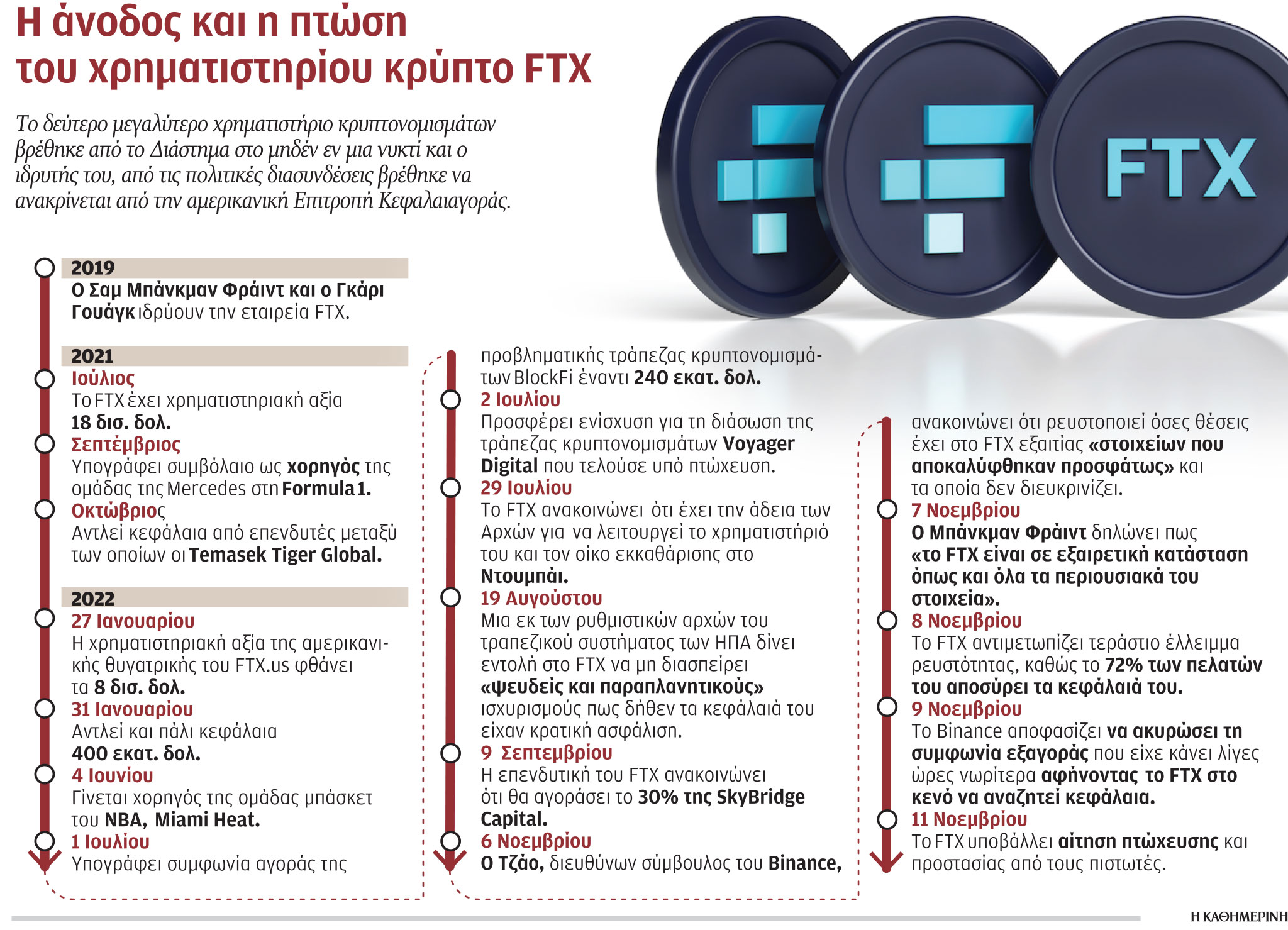

The collapse of one of the world’s two largest cryptocurrency exchanges, FTX, was not publicized and probably will not go as quietly as others. Even if there is an element of exaggeration in the current stereotypical “Lehman crypto”, its fall could prove to be a watershed moment for the industry. And not only because of the strength of this particular company and its large capitalization. Not because of the connections of its founder, Bankman Freed, a 30-year-old who used to appear on international forums unshaven in shorts and at one point last year sought to buy Goldman Sachs and was considered the most established person in the “cryptosphere”. “. There are clearly more serious factors capable of causing the biggest shocks in the industry, such as lack of regulation, opacity, exorbitant price fluctuations. First of all, the fact that it is based on encryption technology, which is quite inaccessible to most people. Even because its purpose is to circumvent the central monetary authorities.

It also didn’t come out as the year we’re going through has been for the most part literally devastating for this industry, which has only captured the attention of the general public for five years or so. Many other companies in the industry have failed, including those that FTX was quick to bail out, such as cryptocurrency banks Celsius Network, Voyager Digital, and BlockFi, as well as “cryptocurrency” hedge fund Three Arrows Capital. It was also preceded by a double-digit drop in the price of cryptocurrencies, with the largest and most popular of all, bitcoin, being capped at around $16,000 of the more than $40,000 it has skyrocketed to over the past two years. The total capitalization of the cryptocurrency market was capped at $900 billion from three trillion. dollars in the corresponding period last year.

It looks like a domino effect has begun on the market, as BlockFi “froze” the withdrawal of funds from its customers.

The drop was a result of the high volatility that stock markets have experienced this year as central banks hiked interest rates, the energy crisis escalated, as did the war in Ukraine, and investors turned away from risky investments.

The question is what to do with depositors’ money, given that, unlike bank accounts, they are not guaranteed by the state and must be claimed in court. Equally poignant is the question of whether there will be any large-scale impact on the cryptocurrency market or the market as a whole, which Moody’s all but rules out. At the time of writing, it seemed like the market domino had already begun as BlockFi, which Buckman Freed bailed out with a $250 million loan, “froze” withdrawals from its clients. After all, not only cryptocurrencies fell, but also shares of companies in their sector, such as Coinbase. After all, in the Bahamas, where FTX is based, the authorities have already “frozen” her assets and appointed an overseer to liquidate her. As for FTX investors, including BlackRock, Ontario Teachers’ Pension Fund of Canada, Sequoia Capital, Lightspeed Venture Partners and SoftBank, all of them could lose their investment. And, of course, the last question: what will be the fate of Sam Bankman Freed, who until a few days ago was the undisputed king of the crypto industry. His personal fortune was estimated at more than $15 billion. However, with the collapse of FTX, his personal fortune has plummeted by 94%, and the US Securities and Exchange Commission is already investigating him.

Beginning of the end of Sam Bankman Freud

Kevin Rose/New York Times

The cryptocurrency industry is known for its spectacular reversals, extreme price swings, and fortunes that come and go overnight. However, even by the standards of the crypto industry, what happened in a week was outrageous. For those unfamiliar with the world of cryptocurrencies, the collapse of FTX, one of the world’s largest cryptocurrency exchanges, is bland and uninteresting news that they will gladly skip over to read the latest adventures of Elon Musk on Twitter. However, in the “crypto” world, it is already being commented on as the “Lehman of cryptocurrencies” by analogy with the collapse of Lehman Brothers in 2008, which caused a global panic in the financial system and became known to ordinary people. The mess on the Wall was at that time on the street.

Indeed, the fall of FTX, as well as rival Binance’s decision to cancel the acquisition, could turn out to be the most dramatic story of the year, a drama involving billionaires, rumors of sabotage, and battles in which the future of this exchange is an industry share. In this story, one of the brightest personalities of the “crypto” world falls from the favor of fortune and many others, whose fall may indicate that much worse days await this industry after this year’s losses. To understand this story, let’s see what happened.

Thus, there are two exchanges where the majority of cryptocurrency trading takes place and they are Binance and FTX. The largest of these, Binance, is run by Chinese billionaire Changpeng Zhao, known in cryptocurrency circles as CZ. Binance’s activities are somewhat obscure. He does not even have official offices, although he has been involved in the investigations of the authorities and supervisory authorities in many countries in which he works. However, it has proven to be extremely successful and currently controls about half of the cryptocurrency exchange market. Based in the Bahamas, FTX is run by Sam Bankman Freed, a 30-year-old American billionaire and Democratic donor. With a market capitalization of $32 billion, it is better known in the US than Binance, in part because it has spent millions of dollars buying stadium rights and hosting high-profile conferences attended by people like Bill Clinton.

After all, FTX is considered – in fact, it was until a few days ago – one of the “large cryptographic capitalization” companies, somehow a stable, well-capitalized business that survived even when the rest of the market was in free fall.

It has spent most of this year supporting other “crypto” companies and is generally viewed by investors as a responsible company that has grown without engaging in risky speculation or gambling with its clients’ funds.

The “New Warren Buffett” and the Mysterious Chinese Man Who “Runs” Binance

Sam Bankman Freed, also known as SBF, rose to fame with the success of FTX and is considered the face of the crypto industry. He is a quirky, unassuming techie who walks around in shorts, athletic shoes and slicked back hair and has earned a reputation as a law-abiding “crypto mogul”. Notably, a recent issue of Fortune magazine featured him on the cover and called him “the next Warren Buffett.”

Changpeng Zhao, on the other hand, is known to be a renegade. He has spoken out against the regulation of cryptocurrencies and many countries have banned Binance as it operates without a license. Under systematic pressure from US authorities, in 2019 Binance blocked US users from accessing its main platform and created Binance.us, a separate exchange legally operating in America. This year, as Washington’s crackdown on the crypto industry began, Bankman Freud and FTX began lobbying Capitol Hill and spending millions to garner the support of cautious lawmakers for crypto-friendly rules.

This attitude has caused a split in the “crypto” world. Some of their fanatical supporters have come out in support of the regulatory effort. Others, however, have accused Sam Bankman Freed of trying to undermine the rest of the crypto industry by pushing through laws that would cripple his competitors and leave FTX unscathed. Binance CEO Zhao was among those who opposed efforts to regulate the industry. He was once on friendly terms with Banchan Fried and Binance invested in FTX. But the two businessmen came into conflict because they had different goals. And now they are arguing about it.

Last week, online news outlet CoinDesk reported that hedge fund FTX, Alameda Research and FTX, while supposedly separate businesses, are actually closely related. Some cryptocurrency watchers believe that Zhao and Binance are behind the leak, that they deliberately leaked the document to question the stability of FTX. However, Binance denies this. Zhao then announced that Binance would sell all purchased FTX cryptocurrencies. Fearful of losing their money, investors withdrew more than $6 billion from FTX in three days, leaving the company desperate for liquidity to meet its obligations.

Bankman Fried tried to reassure investors with tweets that “FTX is in very good shape” and that “some competitor is trying to undermine us by spreading false rumors.” But the panic continued, and after several unsuccessful attempts to secure an infusion of capital from private investors, Bankman Fried announced that he would sell his company, minus its US division, Zhao and Binance. However, on Wednesday, Binance changed its mind and announced it was pulling out of the deal after reviewing the company’s filings and finding that “FTX’s issues are beyond our control and we cannot help.”

And it all unfolded in real time on Twitter, with both Zhao and Bankman Freed active on it. By the way, Zhao was a partial owner of Twitter a few days ago, since Binance invested about $500 million in its acquisition by Elon Musk. Meanwhile, employees and investors tried to figure out what had happened, and Fried, a banker, apologized in a letter to investors for not taking more effective and more preventive measures in time.

Lori Barajas is an accomplished journalist, known for her insightful and thought-provoking writing on economy. She currently works as a writer at 247 news reel. With a passion for understanding the economy, Lori’s writing delves deep into the financial issues that matter most, providing readers with a unique perspective on current events.