While Turkey as well as Tayyip Erdogan in full swing towards the elections of 2023, when the majority of the Turkish people experience poverty, accuracy as well as energy crisis, analysts and economists do not cease to be surprised by the juggling of the Turkish president. Tayyip Erdogan manages to create a seemingly positive image in many aspects of the Turkish economy, although in them its pathologies are already emerging, and he is ready to attack anyone who comes out the winner in the elections.

Turkey’s foreign exchange reserves are again in negative territory.

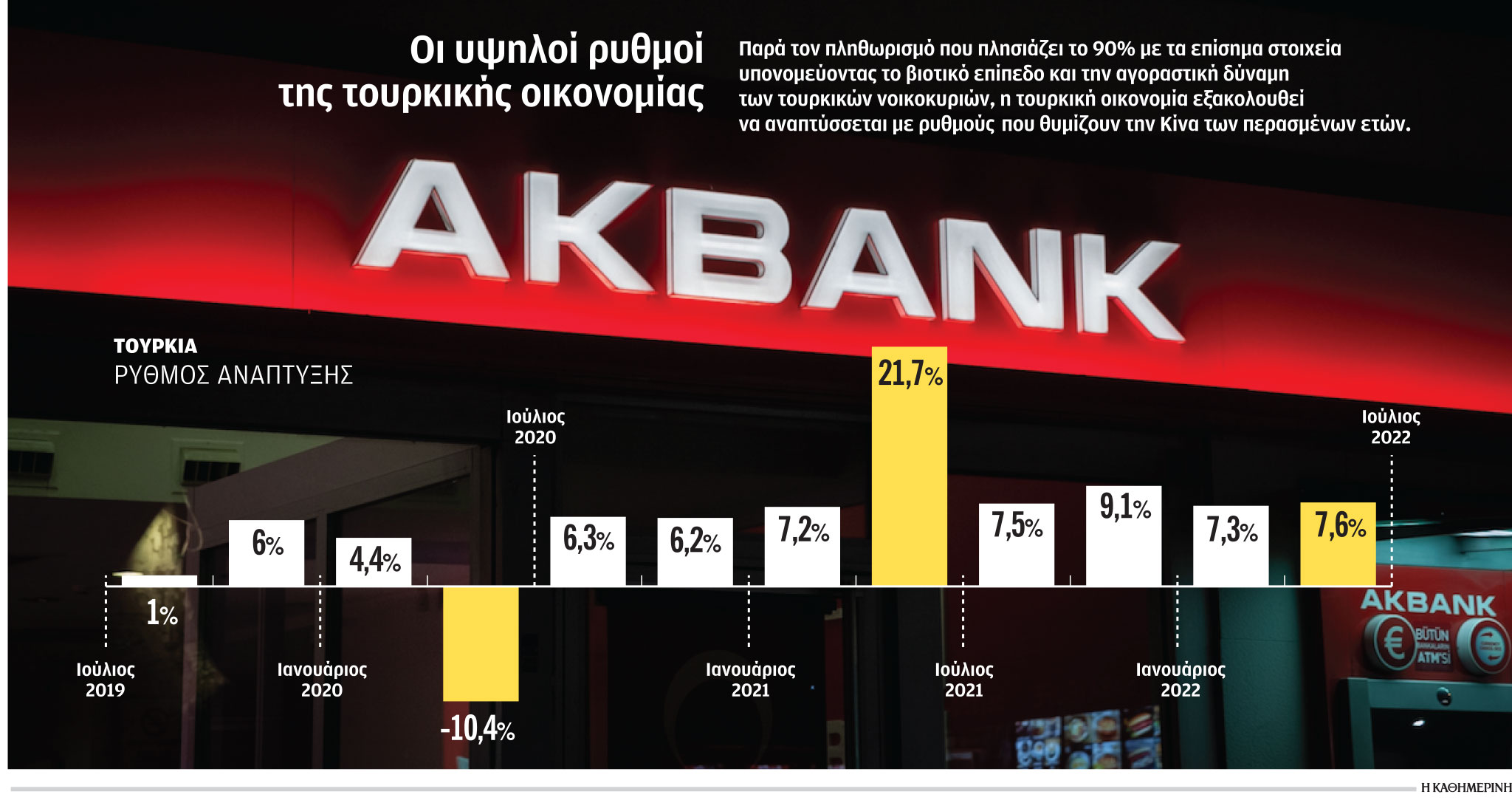

HOUR Turkish economy shows a pace reminiscent of China of the last decade: data for the second quarter shows that Turkey’s GDP grew by 7.6%, and growth in previous months exceeded 7%. In the second quarter of last year, in fact, with the lifting of restrictive measures against the pandemic and the restoration of tourism, the Turkish economy recorded a leap forward with a growth of 21.7%. In a year of major market turmoil around the world, Istanbul’s stock market posted impressive gains, with the Borsa Istanbul-100 index up 144% in local currency and 73% in dollars.

Erdogan’s latest tricks were leaked within a week that it was revealed that Ankara’s deal with Riyadh was in the pipeline for a $5 billion infusion of foreign exchange from Saudi Arabia. It will be an impressive pre-election maneuver, as the gap created between the two countries four years ago by the assassination of Saudi journalist Jamal Khashoggi at the Saudi Arabian consulate in Istanbul is supposed to be bridged. With a difference of one day, it became known that Ankara is once again receiving a new strong injection of capital from Qatar, which will provide it with capital of 8 or possibly 10 billion dollars, for the second time in just two years. In 2020, she provided her with about $15 billion. In the meantime, Turkey’s foreign exchange reserves are backed by $5-10 billion that Russia has provided to it for the construction of a nuclear power plant, and at the same time, Turkey acts as a conduit for Russian oil to enter Europe. Indeed, in recent years, Ankara has concluded a number of currency exchange agreements with its allied countries, such as China and South Korea. However, the reality is not so good. Bank of Turkey foreign exchange reserves fell again to $11.5 billion. According to Goldman Sachs, from March to September alone, the Bank of Turkey spent at least $17.9 billion to support the Turkish currency. Despite successive foreign exchange injections, they are back in negative territory as the Bank of Turkey owes $47.6 billion in short-term loans to Turkish banks, as well as $23.6 billion borrowed from other central banks. In short, even 11.5 billion are some kind of virtual ones. And yet in 2011, when the Erdogan government followed some rules of prudent economic policy, the reserves of the Bank of Turkey stood at $71.1 billion.

Debt juggling and stock trapping

Another clever move by Erdogan to keep banks’ borrowing costs artificially low is the obligation he placed on Turkish banks to buy large amounts of Turkish government bonds. About three weeks ago, he ordered banks holding less than 50% of their deposits in Turkish lira to increase their holdings in Turkish debt by 75%. Some old rules require banks to hold Turkish debt as collateral. These forced placements by Turkish banks have created an artificial demand for nearly $5 billion worth of Turkish government bonds.

As a result, Turkey’s 10-year government bond yield fell about 1,550 basis points to 10.5% from a record high of 26% for the year. In short, they thus reduced the cost of government borrowing, which is projected at 4.47 trillion in the next year’s budget. Turkish lira, an amount equivalent to 240 billion dollars. In practice, however, Turkish banks, which have traditionally been a strong pillar of the Turkish economy, are at risk due to the forced accumulation of Turkish debt on their balance sheets.

As for the dizzying rise of the Istanbul stock market, it actually hides one of the most terrible pathologies of the Turkish economy: inflation that has soared into the “stratosphere”, since according to official data it is already approaching 90% and moving upwards, while a group of independent Economists ENAG calculated that it is 176%. And of course, on the orders of Tayyip Erdogan, the Bank of Turkey does nothing to stop its dizzying growth, but on the contrary, constantly reduces the cost of borrowing. During the week, for the fourth time since April, Turkish Lira interest rates were cut to 9%.

In fact, local retail investors are flocking to Turkish equities in an attempt to protect their holdings from the continued decline in their value. The truth is known to economists, but opposition leader Kemal Kılıçdaroğlu stressed it last Sunday. In a message via Twitter, the Turkish politician tried to warn retail investors, stressing that “you go into the stock market to protect your savings from inflation, but the real lure is high stock prices.” He even predicted in particularly dangerous tones, without specifying whom exactly he had in mind, that “they are preparing to rob small investors.” Kemal Kilicdaroglu, one of Erdogan’s main opponents in the 2023 presidential election, even said that the Securities and Exchange Commission and the leadership of Borsa Istanbul “will be held accountable” for failing to protect investors.

Ten years of maneuvers to keep the Turkish president in power

In fact, the economic policy pursued in Turkey over the past decade, in fact, since 2013, is full of maneuvers and manipulations on the part of Erdogan, since it is not related to the development strategy, but serves expediency: the stay of the Turkish President in force. That is, what presupposes the preservation of at least seeming economic stability until the relevant elections and, if possible, high growth rates. Therefore, the government is using the most opportunistic methods, intervening many times in extinguishing fires, and so far it seems to be succeeding. And if, until recently, public opinion polls led to the first defeat of Erdogan, then recently the opposite has been true.

2013 was a critical year for Turkey, which, like other emerging markets, left foreign capital when the Federal Reserve began raising interest rates. Since then, the most unorthodox and unheard-of methods of indirect capital control have been introduced in Turkey. Among them is the obligation of exporting enterprises to sell at least 40% of their foreign currency to the central bank in order to support the currency. As part of the same effort, businesses and banks are given access to cheap Turkish Lira loans only on the condition that interested businesses do not buy foreign currency. Cheaper term loans from banks are offered to large enterprises only if their foreign exchange holdings are less than 10% of their annual sales. All these unorthodox, at least to some extent, methods slowed down the dollarization of the Turkish economy and somewhat stopped the aggressive outflow of capital from the country. One of Erdogan’s latest ruthless measures was a quick 50% pay rise he promised around this time last year, but it was short-lived as soaring inflation wiped out all gains. The other was a commitment made by the government about a year ago to replace the percentage deposits they lose as a result of the devaluation of the Turkish lira, but on the condition that they remain in Turkish lira. This latest promise, like others, temporarily stabilized the currency and the economy. In the meantime, Erdogan managed to put forward new theories about the “sinification” of the Turkish economy thanks to the cheap currency, which actually fell, but, according to Erdogan, should have led to an increase in exports, an influx of investments and the creation of new jobs. So far, however, high growth rates have been achieved, but not by increasing exports and not by creating new jobs.

More than 75% of Turks struggle to provide themselves with basic necessities, food and essentials, and pay their rent, according to a survey by the Yoneyl Social Research Center. After all, the Turkish economy is under pressure from external factors, such as, for example, the war in Ukraine, which increased the cost of imports, energy and goods. Meanwhile, major central banks are raising interest rates again, which will soon drive up Turkey’s borrowing costs. European economies have cut or stopped bookings as they head into recession. In short, the balance of the Turkish economy is unstable and is expected to falter in the next major external shock.

Warning

“You buy shares to protect your savings from inflation, but in reality these inflated prices of Turkish shares are a lure,” Turkish opposition leader Kemal Kılıçdaroğlu warned a few days ago of those who were seduced by the high prices of Turkish shares and riskier ones. tons added that “preparing to rob small investors.

Overheat

Commenting on Turkey’s strong growth, Timothy Ash, Emerging Markets Specialist at BlueBay Asset Management, recently noted that “growth is too high, domestic demand is too high, imports are too high. Everything is overheating.”

Big loss

Che Uvat, an economics professor at the University of Greenwich, stressed that “the loss of talent that Turkey is experiencing due to hyperinflation could hurt the country’s economy in the future as it loses the jobs and businesses that could have created these young people.” .

Lori Barajas is an accomplished journalist, known for her insightful and thought-provoking writing on economy. She currently works as a writer at 247 news reel. With a passion for understanding the economy, Lori’s writing delves deep into the financial issues that matter most, providing readers with a unique perspective on current events.