Sell it ATM network located outside the bank branch, study banks in an attempt to further reduce their operating costs.

These are the so-called off-site automatic transaction machines, i.e. those that are located outside the banking network, such as, for example. in department stores, supermarkets, etc. as well as in remote locations throughout Greece, which are not of commercial interest to banks, but serve the local clientele.

In addition to ATMs located in busy, mostly commercial areas or in places with heavy tourist flow – hotels, metro stations – and are profitable, the number of ATMs located outside the office, for example, in hospitals, municipalities and other places serving remote islands and regions of the country and their content is detrimental to banks. The problem in this case is that their sale would have to ensure their continued operation in order to continue serving the residents of these areas, which cannot be discounted.

The second main concern is that selling them will likely increase the fees paid for interbank transactions by residents of those territories, and thus the ATM network will no longer be a cheap transaction point, especially for those territories that banks face. as special cases and are currently exempt from fees.

These are also the reasons why out-of-office ATM sales, despite the fact that this idea has occupied banks for several years, has not yet been realized. Indeed, in recent years, banks have attached great importance to the closure of physical branches and the reduction of staff, so the ATM network has increased or remained stable. A start is expected to be made by Piraeus Bank, which is considering selling its network of ATMs outside the office, but all four systemic banks are in similar thoughts or discussions.

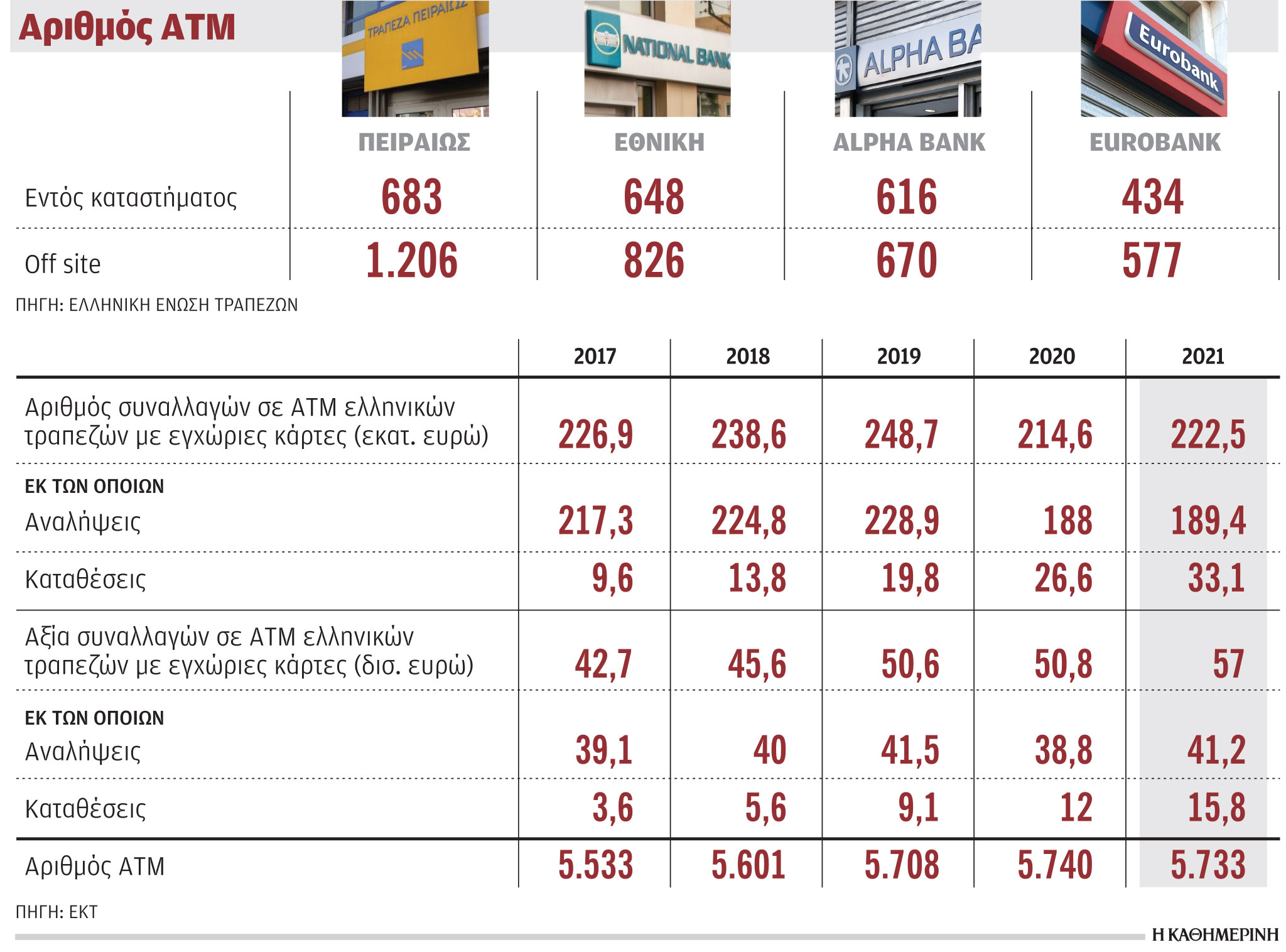

According to the Hellenic Banks Association, the network of third-party ATMs has 3,346 outlets, of which 3,279 are in four backbone banks. The number of ATMs outside the office exceeds the number of ATMs located in bank branches, while, according to EET data, most of them, i.e. 2046 out of 3346 are located outside the country’s two major prefectures, Attica and Thessaloniki.

The high cost of maintaining, supplying, guarding machines in department stores, supermarkets, hospitals, etc.

In the opinion of banks, the maintenance of this network of ATMs, i.e. their leasing, their supply and their protection, is a significant cost for banks, and an additional cost factor is the increase in theft phenomena, which are observed mainly in ATMs in operation. outside of bank branches, but also the growing security obligations they will have to fulfill, making their job extremely costly.

Another key reason why the discussion about their sale has returned to the fore is the significant increase in electronic transactions, mainly through the Internet and mobile banking, which are replacing not only transactions in a physical store, but also through ATMs. which, nevertheless, continue to serve 45-48% of cash transactions in the country.

In any case, ATM usage is declining or, at best, increasing at a much slower rate than those displaying the most advanced digital channels such as Internet and mobile banking, which are growing at rates of 10% and 45%. % respectively. This is another reason for the gradual obsolescence of ATMs, especially those installed on the street and not as modernized as ATMs in stores, which now serve complex transactions.

According to the ECB, the number of transactions carried out at ATMs of Greek banks increased from 214.6 million to 222.5 million transactions in 2021, but this seems to be temporary and is mainly due to the fact that 2020 as a year of comparison is not representative due to the pandemic.

Decrease in transactions

Comparison with the immediately previous year shows that the number of transactions in the period 2019-2021. decreased by 10.5%.

It is also noteworthy that their use for cash withdrawals has decreased, while for cash deposits, on the contrary, it has increased. This is due to the fact that more and more citizens are no longer resorting to ATMs to receive money, since a significant part of the purchases are now made by bank transfer of the account or using a debit or credit card.

Source: Kathimerini

Lori Barajas is an accomplished journalist, known for her insightful and thought-provoking writing on economy. She currently works as a writer at 247 news reel. With a passion for understanding the economy, Lori’s writing delves deep into the financial issues that matter most, providing readers with a unique perspective on current events.