A suitable period for making decisions in her field saving it’s considered what we’re going through like returns proposed today term deposits and which range from 1% to 2% depending on the duration and amount, include an increase in interest rates and therefore no more aggressive action is expected in the near future.

Estimated time for current interest rates starts the countdown, as the perturbation on markets the previous period and especially the trend of its de-escalation inflation justify abstaining from central banks regarding their next steps, with a slight increase in the coming months and interest rates stabilizing at 3.55% at the end of the year. Already, the 12-month euribor, which reflects the forecast for the next twelve months, has been on a downward trajectory since the beginning of March, which, according to estimates, also indicates a halt in interest rate growth.

Interest rates on time deposits, after being increased by banks over the past two months, are scaled quarterly or depending on the amount. The policy of each bank is different: the National Bank prefers to basically maximize the yield depending on the amount, however, starting with small amounts of 3,000 or 10,000 euros, while other banks, such as the Eurobank, also start with small amounts, such as 10,000 euros, while focusing on maximizing quarterly performance. Alfa-Bank maximizes returns on deposits over €30,000 by combining both amount and duration, offering higher returns for amounts over €100,000, a policy followed by Piraeus Bank that also maximizes returns quarterly and for comparable amounts. Based on the tariffs of banks, the profitability of amounts up to 100,000 euros, constituting an average savings, fluctuates on average within 1.30% -1.50% and always on the condition that the depositor keeps his money in a closed account and does not “take” before the end of the scheduled period, which can be 12, 15, 18 or 24 months.

The yield on amounts up to 100,000 euros varies on average within 1.30% -1.50%, provided that the depositor does not “withdraw” them earlier.

In order to choose a better future, the investor must focus on the weighted average return, since it is this that provides the maximum benefit for his money. This is because the nominal interest rates that banks list on their invoices for each quarter are annualized. Thus, if the deposit reports an interest rate of 1% in the 4th quarter, this means that the actual return is 0.25% in this quarter, i.e. 1/4 block and so on. The key feature of term deposits offered by banks is flexibility, i.e. the ability to withdraw your money before the scheduled repayment date without penalties, as was the case in the past. This feature is applicable to most products and is also the reason for the low yield in the first quarters. In this way, banks seek to prevent the phenomenon of seeking higher interest rates from bank to bank and at short intervals, a trend that has prevailed in the past and especially during periods of limited liquidity in the banking system due to the large outflow that existed during the crisis. years. Today, with deposits close to 183 billion euros, of which 140 billion euros are household deposits, the need to attract deposits, although not underestimated by banks, does not encourage domestic competition with high interest rates for short periods of three or three years. six months. On the contrary, the priority is to maintain the deposit base and customers that each bank has at a reasonable price.

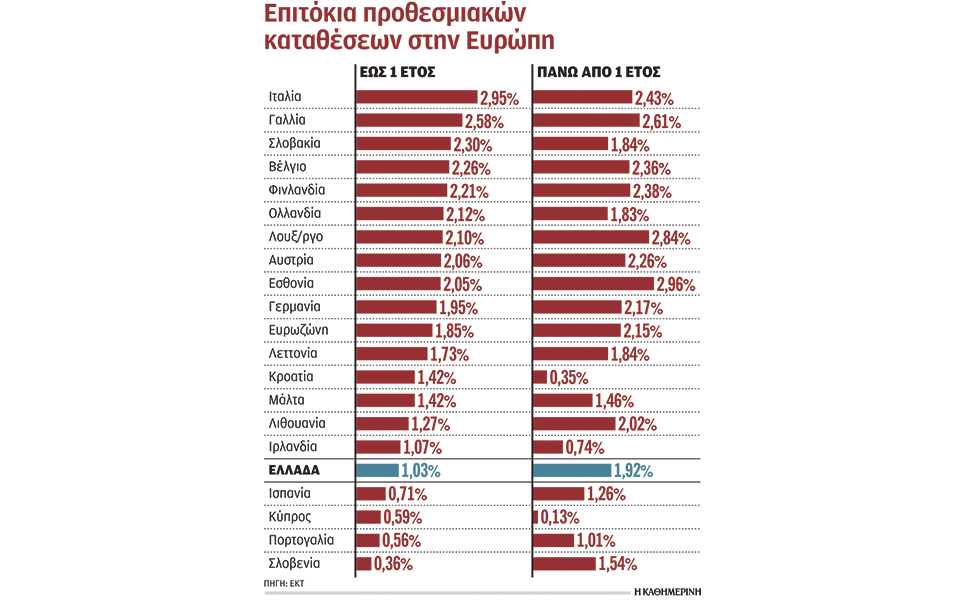

The interest rates on term deposits offered by Greek banks were the same as those of other European countries, but with a focus on term deposits over 1 year. According to the data published by the European Central Bank, the average return on term deposits of this category in our country is 1.92%, compared to 2.15% in the Eurozone, the countries of which show large fluctuations. Approximate interest rate on time deposits for more than 1 year is 2.17% in Germany, 2.43% in Italy, 2.61% in France, and in Portugal 1.01% and in Spain 1.26%. However, Greece remains low on average interest rates on term deposits up to 1 year, which are 1.85% in the Eurozone compared to 1.03% in Greece, with the highest interest rates recorded in Italy (2.95% ), in France (2.58%), and the lowest in Portugal (0.56%), Cyprus (0.59%) and Spain (0.71%).

Benefits of Investing in Bond Mutual Funds

Along with simple deposit products and term accounts, banks and asset management companies are introducing fixed income investment products such as bond mutual funds, aimed at those who are willing to invest their money for a longer period of time, for example. 5 years, with a better dividend yield or additional yield at maturity, depending on the mutual income management that the manager achieves.

Bond mutual funds combine all the benefits of bonds, offering diversification, immediate liquidity, and zero taxation on both capital gains and dividend distributions. According to industry professionals, they can be a component of any investor’s portfolio, regardless of their risk profile, and be used as the main position of a conservative client’s portfolio or to form a more “aggressive” investor’s portfolio, as a counterbalance to sharp price fluctuations. placement of shares.

They are intended for those who are ready to invest their money for a longer period of time, ie. 5 years, achieve the best performance.

“The Greek market has shown it can handle the odds of the times with the help of mutual funds,” notes Eurobank Asset Management Managing Director Theofanis Mylonas. “Since September 2022, when Eurobank Asset Management AEDAK first launched Target, more than 1.5 billion euros.”

Industry experts say that after an unusually difficult year for all investment categories, such as 2022, very attractive levels have been created, especially in bonds. Government bonds are expected to act as a hedging instrument, unlike last year, as their price increases are expected to be driven by a gradual decline in inflation and the peak of the interest rate hike cycle. On the other hand, corporate bonds remain positive as corporate profit margins show no serious deterioration and corporate balance sheets remain strong.

“Buy and hold” strategies for bonds to maturity – TargetMaturity – are a particularly interesting option for additional exposure to a broadly diversified portfolio, as they offer diversification and resilience with the ability to “lock in” an attractive medium-term return relative to other forms of fixed income investment . Among the steps that are expected immediately, as noted by Piraeus AEDAK Managing Director Iraklis Baplekos, “issuance in cooperation with Piraeus Bank from next week of a new A/K bond, Piraeus Strategic Regular Income 2028 (II), which is a continuation of the significant investor response to the previous two A/C, which were organized through the network of Piraeus Bank and raised funds in the amount of 580 million euros.”

On the other hand, the interest yield of bills is also high, which, based on yesterday’s 26-week issue, were valued at 3.15%, while the previous 52-week issue at the beginning of March had an interest rate of 3.75%. Investments in interest-bearing bonds or Greek government bonds have no limit on the amount of the deposit, and income is not taxed for the first 15,000 euros, and amounts over 15,000 are taxed at a rate of 15%, that is, in the same way as income from deposits.

Source: Kathimerini

Lori Barajas is an accomplished journalist, known for her insightful and thought-provoking writing on economy. She currently works as a writer at 247 news reel. With a passion for understanding the economy, Lori’s writing delves deep into the financial issues that matter most, providing readers with a unique perspective on current events.